An index fund is known to be the most powerful investment vehicle to build wealth for everyday investors. Now that the stock market has tumbled from its all-time high, should you invest in one now?

To answer this, we need to first understand what an index fund is and determine if it fits with our financial situation.

Let’s explore this topic today!

This post may contain affiliate links, which means I may receive a commission, at no extra cost to you, if you make a purchase through a link. Please see my full disclosure for further information.

Also, this post is for informational purpose only and shall not be construed as financial advice. All investment carries risk therefore please invest responsibly. Here is my full disclaimer.

What’s an Index Fund?

First thing first, an index fund can be either an index mutual fund or an ETF (exchange-traded fund). While an index mutual fund is a type of mutual fund, an ETF is a type of security.

These index funds can track any index on a specific financial market such as the S&P 500, total stock market, and total bond market. Most of these funds pay dividends/interests.

For the purpose of investing, you can buy either an index mutual fund or an ETF tracking the same index (e.g. S&P 500) and they will function very similarly.

One notable difference is the timing of share price captured.

For example, an index mutual fund share price is captured at the end of the day while an ETF (since it’s traded like stocks) can be purchased throughout the day at different pricing.

For a long-term investor (we’re talking about 10+ years horizon), it makes very little difference to buy a mutual index fund or an ETF. One small difference may be the fee structure by one basis point depending on the fund (see “Fee Structure” below.)

However, if you’re a day trader, then buying an ETF has certain advantages. But for the purpose of indexing, a passive investment strategy, both an index mutual fund and an ETF will follow the performance of a particular index.

Index Fund: A (Very) Brief History

The first public index fund was created in 1975 by John Bogle, the founder of Vanguard. During the inception period, he received a lot of heat from industry money managers who charged exuberant high fees on their managed mutual funds.

Bogle changed the game of investing for everyday investors by offering index funds that charge way less in fees than those of other mutual funds. Overtime, it’s also proven that indexing can beat out most money managers including high profile hedge fund managers in terms of profitability.

This is GREAT NEWS for an average investor because it means that we can have access to investments at a low cost.

Later in 1993, ETF’s were introduced but Bogle was not a huge fan of this since it may encourage people to trade them like stocks.

In his view, investing in an index fund should be done as a buy and hold strategy. An ETF, while it can be a long-term investment in itself, has a certain allure to day traders since one can easily buy and sell at different price point following the daily volatility of the market.

Nevertheless, ETF’s are widely offered in many brokerages including Vanguard.

Why Do People Invest in an Index Fund?

Short answer: Profits.

Without them, NO ONE would invest in anything period.

When you invest in an index fund tracking a broad-based stock or bond market, you’ll earn dividends and interests. In addition, doing so in the long-run means that your investment can grow overtime.

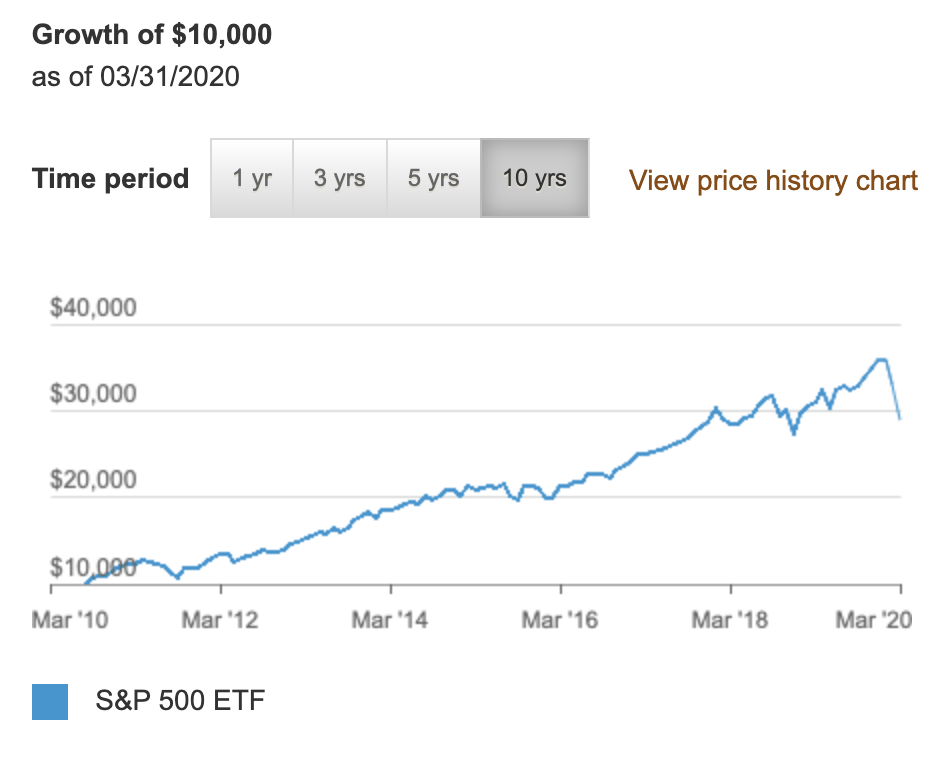

Check out the performance of the S&P 500 ETF in the past ten years with 10.53% average return (including the recent dip):

But the longer answer is that an index fund is known to have a low fee structure. This makes them much more profitable comparing to other mutual funds managed by a professional portfolio manager.

The reason that the fee can be kept so low is because there is way less work (and guessing game) in putting together a fund that makes profits. That’s because it basically takes an index, like the S&P 500, and puts together a portfolio that mirrors it.

And if you ask Warren Buffet, he might tell you, “A low-cost index fund is the most sensible equity investment for the great majority of investors.”

In fact, this is what he had laid out in his will, “Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund.” (Source: Berkshire Hathaway Inc. Letter to Shareholders, 2014, page 20.)

The main reason? Investing in an index fund is easy and affordable.

Main Reasons Why an Index Fund Is a Superior Investment Vehicle

Comparing to other mutual funds, an index fund offers diversification, lower fee structure and the ease of investing. It’s a much more attractive investment vehicle overtime since it’s known that most high-fee managed funds cannot beat an index anyway.

Diversification

One of the advantages of buying an index fund is diversification. This means that when you buy shares of an index fund like the S&P 500, you’re exposed to all the stocks in this index.

This is great because it means that your portfolio is automatically diversified without hand picking individual stocks or bonds.

With diversification, your portfolio can have better chances of earning a higher return while reducing risk. This is especially true during sudden market swings. You just never know which stock will outperform the other, therefore it’s best to buy an index that has a balanced mix.

Low Fee Structure

Because the function of an index fund is to track the performance of a given index, it doesn’t incur as much operating cost as other mutual funds.

An expense ratio is the fee that a fund charges for administrative and other operating expenses in managing a fund. It is also known as MER or management expense ratio and is calculated by dividing the total fund costs by the total assets under management.

For example, the expense ratio of index mutual funds and ETFs at Vanguard charge between 0.03% to 0.93%. Some of the popular index funds have very low expense ratio due to intense competition on the market.

Here are few of the popular low-cost index funds that you can find in Vanguard along with their fees (expressed in %):

- S&P 500 ETF = 0.03% (Admiral Share = 0.04%)

- Total Stock Market ETF = 0.03% (Admiral Share = 0.04%)

- Total Bond Market ETF = 0.035% (Admiral Share = 0.05%)

(Note: Fee data gathered as of April 13, 2020. These fees may subject to change per Vanguard.com.)

By comparison, a typical mutual fund that you find at a bank would charge between 1% – 3%. This is a huge difference in cost comparing to index funds!

Ease of Investing

As mentioned previously, investing in an index fund is a passive strategy known as indexing.

On the other hand, an active investment strategy or active investing requires ongoing research, buy/sell activities, and market timing. This could take a huge amount of work for both experienced and inexperienced investors alike.

Moreover, it has been proven that most active investment strategies cannot outperform an index fund while charging exuberant high fees. This is no wonder why Warren Buffet advocates on indexing rather than stock picking for an average investor.

Should You Invest Now?

It depends – this is not the best answer, I know, but it’s a valid one.

Do you have $1,000, $10,000 or $100,000+ lying around? The amount of available funds you have can be a huge deciding factor for whether or not to invest.

I’ve once had only $1,000 in my bank account in college (sometimes even lower than that!) and I can tell you that these one thousand dollar bills were my livelihood!

It’s certainly different investing while having just $1,000 at your disposal vs. having $10,000+. With a measly sum of $1,000, investing was far from my mind. The risk was just too high!

Furthermore, do you owe any debt? You may want to get rid of those before you start investing as most debts are wealth destroyers.

Related: How to Pay Off a Mortgage in 8 Years (Note: You don’t need to pay off a mortgage before investing)

Simply put, even though you may have $10,000 in your savings account, if you have $19,000 in credit card and student loan debts, then you essentially have -$9,000 in net worth.

Another important criterion is cash flow. Is your job as secured as the Mona Lisa painting in La Louvre Museum? If so, then investing is okay as long as you have ongoing cash flow and excess funds. Otherwise, why not build a side income?

In essence, investing should not be a priority if your main source of cash flow (i.e. from your job or business) is not secured and/or you have very little in funds.

As you can see, the decision to invest really depends on your financial health as well as how well you can stomach a market downturn.

Getting Your Financial House in Order

Generally speaking, if you have a SECURED stream of income enough to cover your living expenses and/or six months of emergency funds with no significant debt, then yes, investing in index funds during a downturn may be a wise decision in the long-run.

Historically, an index fund is known to move upwards and to the right overtime. Even in times of recession, it still yields a small stream of dividend/interest income. Therefore, investing at a low point may mean buying at a discount.

HOWEVER, if your financial house is not in order such that you only have less than $10,000 in reserve, have a significant portion of debt, or both, then you probably don’t want to invest right now despite the “discounted” pricing.

The reason for this is because cash is king and this is especially true during times of uncertainty.

Making the Right Move

No matter how tempting the pricing may seem at the moment, the truth is that it can still go lower. It’s not a big deal if you don’t need to sell. But, if you can’t hold on during tough times, then selling at a low pricing environment would mean that you absorb the losses.

Therefore, while I truly believe in the power of indexing, I don’t think it’s the solution for everyone.

To assess where you stand in terms of your financial situation, read this article on financial goals.

Sometimes, getting your finances in order is not an easy or straightforward process. In this case, it may be worthwhile to seek professional help such as from a fiduciary financial advisor or a trusted financial coach.

A FIDUCIARY financial advisor is legally required to put your interests ahead of his/her own. Not all financial advisors operate this way, so be sure to look for the keyword, fiduciary.

Alternatively, you can also enlist a financial coach who is good at managing finances to take a look at your financial situation. This can be a family member, a friend, or someone you trust.

Even though it cost money to hire a professional, it may be worthwhile if s/he can help you turn your financial situations around or optimize your finances. But if you can’t afford to hire one, then you do have to take matters into your own hand. (Books, courses and personal finance blogs are all helpful resources.)

Can you imagine having money not wisely spent, saved, or invested? This in itself is a loss of income.

After all, your money should always be working hard for you. And once you understand how to do that, you might find that they are in fact excellent workers.

What are some other advantages of investing in an index fund? Do you believe indexing is a good investment strategy? Why or why not?

PIN it to share it

Thanks for sharing such a thorough explanation. Even though I hadn’t previously heard of an Index fund, you’ve certainly made me curious about investing.

Great read! Never even knew this existed

Great, very easy to understand explanation. We have a mutual fund but have been looking at options. Definitely considering now!

Very detailed explanation, I had no idea what an index fund was! Thank you for sharing 🙂

Awesome, glad to share!

Thank you for sharing!! I never knew what an index fund was and you have explained it very well!!

No problem! Glad to hear that you learned something new.