Peer-to-peer or P2P lending has been gaining steam in recent years due to the easiness of opening an account via the web. It’s still a relatively new concept but it’s making its way to the FIRE community.

(FIRE stands for “financial independence; retire early.”)

However, with the recent pandemic, it’s uncertain if the P2P market can survive an economic downturn. That’s because it’s so new that it hasn’t yet gone through an economic crisis.

Should We Invest in P2P Lending?

Today, we have a guest post by Dennis from Spending Consciously who will share with us his experience investing in the P2P market. Dennis is based in the Netherlands so for the purpose of this post, the currency denoted will be expressed in EURO (€).

In addition, he wrote this article just before the pandemic happened. Due to the volatile market, Dennis has decided to put a pause on investing in P2P lending for the time being.

Nevertheless, P2P lending can be a viable investment if it can survive (or perhaps even thrive after) the financial crisis. This period of uncertainty will be a true test for the P2P lending business.

In any case, it is important to note that while investing is a proven way to build wealth, it also comes with a certain degree of risk. Therefore, as you learn more about P2P lending, please be advised that you should always conduct your own due diligence before making any investment decisions. (See our disclaimer here.)

So without further ado, let’s get into P2P lending and what it’s all about. Take it away, Dennis!

This post may contain affiliate links, which means I may receive a commission, at no extra cost to you, if you make a purchase through a link. Please see my full disclosure for further information.

Anyone looking into ways to have their money work for them must have come across what is called Peer-to-Peer (P2P) lending. The words might give some indication of what it is about. But how it works and, more importantly, how it can make you money and maybe help you on your way to FIRE (Financial Independence Retire Early) is not immediately apparent.

In this blogpost we will dive into peer-to-peer lending, how it works, its risks and rewards and my personal experience with P2P lending on Mintos, an online P2P lending platform.

What is P2P Lending?

P2P lending is literally lending money from one peer to another peer, like you lending money to your uncle Joe. This practice has been around for centuries but it has been a niche market for most of the time. At the end of the 2000’s P2P lending took flight when the financial crisis made banks reluctant to offer new loans.

Today P2P lending has become quite popular due to the promised returns and increased accessibility for interested investors. The global P2P industry reached $34 billion USD in 2018 and is estimated to reach $589 billion (!) in 2025.

How Does P2P Lending Work?

Most P2P lending takes place through online platforms where companies (Loan Originators or LO’s) grant loans to their users (borrowers) in which other users (investors) can invest.

There are individual LO’s and independent companies that run these platforms where the platform acts as a sort of marketplace.

To get started with any platform you’ll have to create an account, go through an identification process and once the account is set, you can transfer funds and start investing in loans. You can invest manually or automatically.

Mintos: One of the Leading P2P Lending Platforms

One of the P2P platforms that I personally use is Mintos.

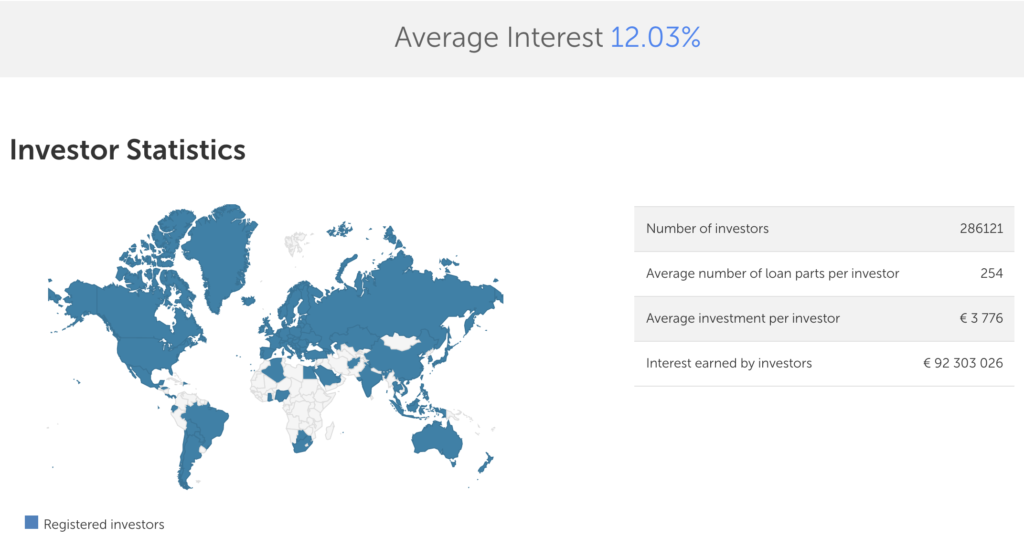

It is one of the leading P2P lending platforms in Europe and it is open to investors from all over the world. According to their own statistics, they have over 280,000 investors who collectively earned €92 millions in interest with an average 12% in return.

The company was founded in 2015 with their headquarters in Latvia. According to their website, “70 lending companies from 33 countries” place loans on the Mintos platform.

The automated investment options with Mintos are Invest & Access and Auto Invest. The latter requires you to create portfolios after which the portfolio will auto-invest in loans.

The Primary Market and Secondary Market are where you can go to manually select loans to invest in.

With auto invest usually comes the option to automatically re-invest your funds for you. This is a great time-saver! Picking individual loans can be time consuming. Time is money!

If all goes well, the process is pretty simple. You invest in a loan, the borrower repays the loan and the funds find their way back to your account where you can either reinvest or cash out.

But…

Risks and Rewards

Not everything goes well.

In order to get those sweet financial gains of P2P lending, in the form of returns on your investment and maybe some platforms cashback and referral offers, you’re exposed to some risks.

Defaulting borrowers

Borrowers default. Many LO’s offer buyback guarantees on loans which means that if a borrower is over 60 days late in its next payment, the loan is repurchased by the LO. However, buyback guarantees are not bulletproof. If an LO defaults it won’t be able to repurchase a loan despite a buyback guarantee.

Defaulting LO’s

There are several LO’s out there with a poor financial performance and equally bad financial positions. Some have no proven track record and/or haven’t made their financial information available. Prior to investing in an LO, do your research. Once you’ve invested you need to periodically review your portfolio. If you choose to rely on other parties for your due diligence, find an independent source. One resource I use is Explore P2P.

Defaulting platforms

A lending platform can default as well. There can be several reasons for that; bad management, bad business model, too many investors withdrawing money, fraudulent activities. A very recent occurrence of such a default is Kuetzal, which seems to have been involved in fraudulent activities. I highly recommend to google Kuetzal to get an idea of scams in the P2P world.

An economic downturn or changing legislature can increase the likelihood of these events happening. Recently the government in Kosovo revoked the lending license of Monego (LO) which put them in deep financial trouble. Bad news for investors!

These risks make diversification across platforms, LO’s and loans, with the necessary due diligence, essential.

P2P Lending Platforms

So what is out there? A great number of platforms. My own experience is limited to the only platform I’ve used so far at the time of writing this post. So I’ll piggyback on the opinion and experience of ExploreP2P.

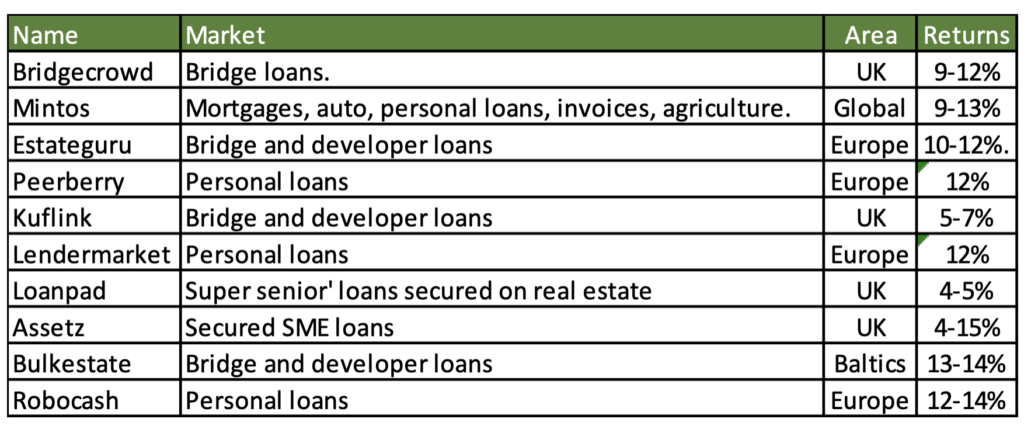

ExploreP2P is a blog and website that compares and reviews P2P websites and platforms. The table below shows ExploreP2P’s 10 favorite platforms.

As you can see, the markets and areas where these platforms operate in differ; there are car loans, real estate investments, personal loans and so on. The good thing about this is that you can choose a market that you feel comfortable with investing in. Or all of them if you don’t really care.

Returns in P2P Lending

The returns that P2P lending offers are very interesting for retail-investors. A year on year return of 10 to 12 percent is not unusual and that makes it an appealing industry to invest in. On Mintos I’ve seen returns on individual loans range between 5% – 20% so the returns for some of the platforms in the table are likely based on a well-diversified portfolio.

The higher the return the higher the risk, so don’t get googly eyes when you see 20% returns being promoted on a platform. That being said, high returns are what got my attention in the first place. I only spend a few hours reading blogs before deciding I wanted to give it a try. There was one blog in particular where an investor laid out his investments with several platforms and showed that he had over €1.000.000 invested in Mintos. Reading his blog gave me the confidence to step foot in the P2P realm myself.

My Investment and Returns

I first started out investing in Mintos because it has been around for several years and is positively reviewed by many users. My initial investment was €1.000. As I got familiar with the platform, I increased my investment to €11.000 within 2 months. I’ll have to admit that that decision was fueled, in part, by the cashback carrot still dangling in my face.

So far, I have focused mainly on short term loans (1-3 months) and I’ve set up investment portfolios for individual LO’s. I like the flexibility to pull out in a relatively short amount of time. Additionally I can sell off investments on the secondary market (with a discount) if I need the money or if I want to leave P2P lending altogether.

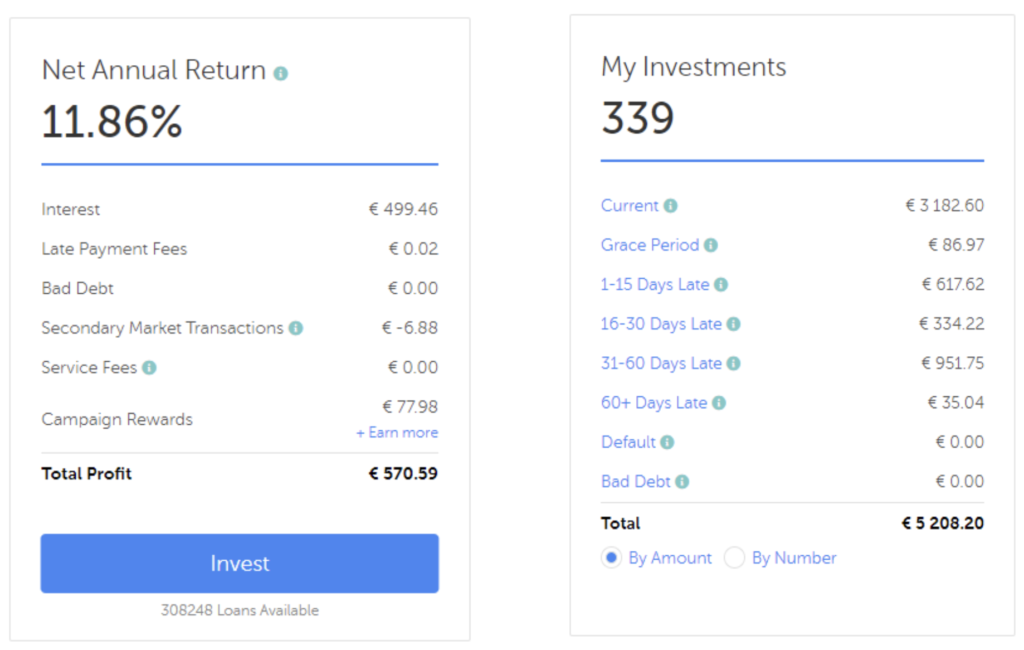

Mintos conveniently tells me I’ve made €570,59 so far in 7 months, an 11,86% net annual return. See the screenshot below on how this is built up.

I believe the net annual return is based on the amounts actually invested. It doesn’t take in to consideration the amount of money that hasn’t been invested during these 7 months (which has been over €3.000 at times).

I also have some bad loans still in my portfolio worth €35. There are the loans under 60+ day late. Mintos could earn some points if they would transfer this to Default and Bad Debt so it would be presented accurately in the Net Annual Return.

There are 2 other LO’s in my portfolio that recently lost their lending license in Kosovo. These loans are listed under 31-60 days late. So far it seems that these loans will be repaid. My exposure there is €208. Even if this would materialize, I would still be up €327.

Time is Money

So how does that relate to time spent? How much time you spend managing a P2P lending portfolio is up to you. But, the amount of time you spend should be directly related to the size of your investment. After all, time is money and if you spend several hours per month calibrating a portfolio of a €1.000 at 12% interest, you’re making less than minimum wage. Which is fine if you enjoy it, but it beats the purpose.

It’s not an invest-and-don’t-look-back type of investment like an exchange-traded fund or ETF. I spend an hour or so per month to review how my investment is doing and adjust my portfolio if necessary. Of course you can perpetually re-invest your funds through auto-investing which will limit the time you spend on managing the investment.

But I believe you should still periodically check in on your investment. What if auto-invest hasn’t been working properly and your money is just sitting there idly? Yes, that has happened to me.

Lessons Learned

Sometimes auto-investing isn’t possible. This could be due to a technical issue, but it is also possible there are no loans on offer that match your auto-invest settings. And so your money is not invested; Another reason to check your investment periodically.

What I also learned is that you can’t rely solely on information that is provided by a platform itself. Mintos isn’t always straightforward in its communication. I’ve sold loans of an LO based on information I gathered elsewhere and consequently the LO in question turned out to have problems.

Every platform has an interest in keeping its business going and can be tempted to keep certain information behind closed doors if they perceive it too risky to share it (read: it might cause investors to run for the door).

Don’t blindly believe the rating given by a platform either. Some red flags to look out for with a LO are negative equity positions, no recent financial statements and a young (and probably inexperienced) management team. That’s why I also rely on more independent sources such as ExploreP2P.

Be cautious with cashback promotions by LO’s. Do some research on the LO offering the cashback first. Some require you to invest in long-term loans, which could be an indication that they have liquidity problems.

Conclusion

With the P2P market expected to rise to over half a trillion dollars, the industry seems to be here to stay. But with the unprecedented pandemic crisis happening, it’s uncertain if P2P can survive during this period.

Since it hasn’t been tested out if P2P lending as an industry can successfully navigate through a financial crisis, I don’t see it as THE way to achieve FIRE. A lot of LO’s operate in countries where legislation might not be what you expect it to be and scams can lurk around the corner.

My final take-away? Always do your research on LO’s and platforms and try not to be the first to give a new platform a try with your hard-earned money. This would allow you to diversify and minimize your risk exposure while having a better chance of making a moderate return!

Author’s Bio

Dennis is specialized in finance in the public domain with a degree in economics. He started his path to FIRE in 2019 while exploring the possibilities of living as a digital nomad. He now works as a financial coach and freelance consultant.

To learn more about Dennis or his coaching business, please visit SpendingConsciously.com.

Subscribe for New Updates from Mama Bear Finance:

Do you invest in P2P lending? If so, on which platform? Do you think the P2P lending business can survive through a financial crisis?

Love it? PIN it

This is very new information for me. Thank you so much!

Glad to hear that you learned something new 🙂

Great read. I’ve heard of this type of investment but didn’t really know how it works. Thanks for the information- very helpful.

That’s great! Thanks for dropping by 🙂