How would you respond if someone told you, “You’re FIRED”?

My response would be: Yessssss, congratulations to me!

No, no, it’s not what you think. FIRE nowadays has a different meaning (it’s short for “financial independence; retire early”). Gone are the days when getting “fired” means getting the pink slip; In the modern world, it signifies freedom – financial freedom to be more precise.

If you haven’t heard about the ‘FIRE movement‘ yet, then you’ve been missing out. But luckily, you came to the right place so let’s find out what this hype is all about and how you can achieve financial independence.

(Spoiler alert: You’re going to get light up!)

This post may contain affiliate links, which means I may receive a commission, at no extra cost to you, if you make a purchase through a link. Please see my full disclosure for further information.

Hello, FIRE

The FIRE movement, known as Financial Independence Retire Early, is a popular notion whereby anyone can quit work and live a more fulfilled life without financial worries.

Before I learned about FIRE, I was unconsciously on the path towards achieving it just by being intentional with my spending habits. I was glad to learn that I wasn’t the only odd ball who actually enjoys living a frugal, minimalist lifestyle.

In order to become “FIRE’d,” one must have accumulated a sizeable net worth that would spit out constant income enough to cover all expenses indefinitely. This would effectively render a traditional 9-5 job optional.

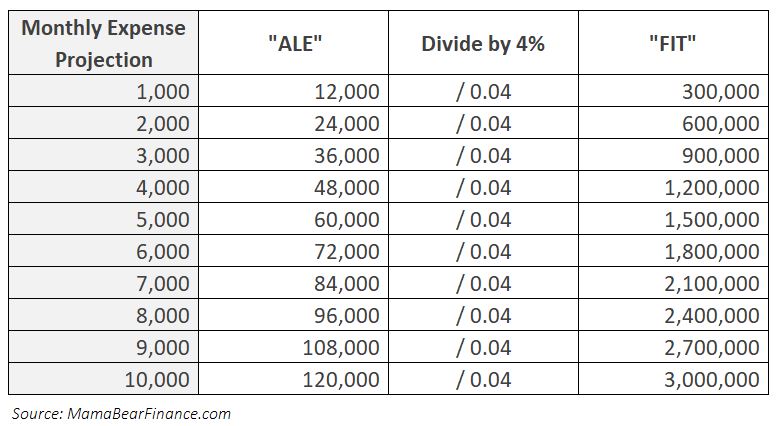

Here are four simple steps you can follow to calculate and reach your financial independence target (or FIT):

Step 1: Know your spending

First, figure out how much expenses you incur each month, then multiply that by 12 to get your annual spending. This is known as the annual living expenses (or ALE).

You can do this by tracking your expenses every month including all fixed and variable expenditures. (Note: Fixed expenses are costs that generally do not change such as rent and insurance premium; Variable expenses are costs that are controllable by you such as your grocery bills, entertainment, and the clothes you buy for your baby).

Step 2: Calculate your nest egg

Once you have your ALE, you can divide that by 0.04 which is also known as ‘the 4% rule,’ and BAM, you get your financial independence target (FIT).

To show you some practical examples, here is a projection of possible FIT amounts based on your spending needs. Notice that if you’re an extreme frugalist who spends below $3,000/month, then your financial independence target is just shy of $1 million.

This FIT, which is also your retirement investment portfolio, is your ultimate prize to reaching financial independence.

Okay, backtrack. What the heck is the 4% rule and why do you divide that by the ALE? (Entering… steps 3 & 4.)

Step 3: Invest in the long-term

The 4% rule is the general percentage that you can withdraw from your FIT and you’ll be able to outlive your portfolio without running out of money.

To understand where the 4% rule came from, I recommend reading the Trinity Study which aims at determining a safe withdraw rate from a stock retirement portfolio for when you hit that FIRE button.

The key here is that your FIT is actually a combination effort of your diligent savings over the years PLUS the accumulated investment effect. It’s important to note that even if you actively save money in your bank’s saving account, your nest egg will most likely be outpaced by inflation, meaning the 4% safe withdraw rate doesn’t apply if you don’t invest*.

“Compound interest is the 8th wonder of the world” – Albert Einstein

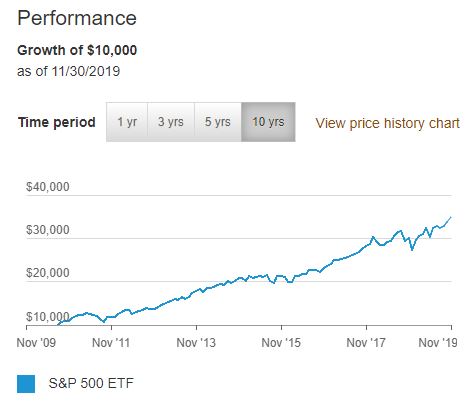

The most popular investment vehicle that is complementary to the 4% rule is a broad-based index fund like the S&P 500. This investment is known to yield an average of 7% in the long-run (e.g. 10 years) which is enough to cover the 4% withdraw rate plus inflation.

Check out the performance of the Vanguard S&P 500 ETF (exchange-traded fund) from 2009 – 2019 as an example.

Therefore, the key takeaway of how you can achieve FIRE is through accumulating savings diligently (and early on) so that this money can be invested and increase in value at an exponential rate of growth through compound interest.

Step 4 (The Final Step): Stay on track

Putting this all together, the formula to achieve financial independence is simply: FIT = ALE / 0.04 (or ALE = FIT x 0.04). This means that if you can pinpoint exactly how much you need in monthly expenses, then you can figure out your nest egg amount to become financially free.

This formula is also useful for keeping you on track in the event that your expenses change overtime. It can provide you a realistic update of how much you’ll need to enlarge your nest egg if you ever decide to spend more.

Therefore, the secret sauce to achieve FIRE in a rapid speed is to target a high savings rate. Most of the people who succeeded at reaching FIRE in their thirties or forties (yup, you read that right) normally save about 50% or more of their income.

Even if you don’t plan on reaching FIRE early (or you’re still sceptical of its viability), using this formula as a guide for your savings rate can still keep you on track.

On the other hand, if you are convinced by this method and are determined to reach FIRE someday, then the simple strategy you can implement today is to increase your income, decrease your spending, or better yet do both, then invest the difference.

(*There are numerous ways to invest your nest egg and they deserve a post of itself. Stay tune for various investment ideas, insights, and opportunities to be uncovered in this blog. Don’t forget to SHARE, comment, and subscribe.)

FIRE Without the “RE”

Although I completely resonate with the habits of FIRE enthusiasts, whose goals are to save money rigorously in the beginning years in order to retire ultra early, I’m not sure retiring early is my ultimate goal.

I understand the RE (retire early) is the most controversial part of FIRE and everyone has his or her own definition of early retirement. Though there is value in RE, I want to focus more on FI (financial independence).

Instead of retiring by age XX, I just want to have the option of doing anything I want with my time while having a steady cash flow. The keyword here is ‘option.’ Having the option to do whatever I want is what gives me joy (and security).

In the present time, having the option to live comfortably while seeing my daughter grow would be the ultimate dream.

However modern lifestyle requires moms to go back to work immediately, because most of the time, one income is just not enough. Therefore most parents do not have the option of staying home to spend longer time with their baby or to fully become a stay-at-home parent.

Though I enjoy working a corporate job (at times), I certainly find that the current maternity leave is way too limited for the benefit of the society. I truly believe that newborns need the nurture and presence of their mothers during the first six months of life.

Therefore having option is really valuable, especially if as time goes, I want to spend longer time with my baby than originally planned. To achieve this, I would first need to establish a stable cash flow to ensure that I don’t have to worry about sustaining myself and my family through a paycheck.

That or we’ll have to tap into our savings account, which is not ideal.

So having the optionality to FI is such a breath of fresh air. This gives me hope that someday I will have that possibility to work as I wish or to take care of my baby without having to worry about money.

Achieving FI with A Baby

Achieving financial independence or FI is no small feat. It requires strong commitment to set achievable goals and then to be laser focused in achieving said goals.

Although increasing income is the hardest part of FI, reducing expense, on the other hand, is much more manageable. After all, the most important objective is to increase savings rate, which can be done by adjusting either side of the variables.

On one hand, I know that having a baby will affect our savings rate, but I’m not totally sold that it would strain our finances. To do this, I started to track my expenses and inventory to ensure that I’m not overspending on baby items.

My hypothesis was that if I could keep baby spending under control, I would have the joy of raising a child without having to derail my FI goal.

So far tracking all of the expenses have given me perspective in how much it costs to raise a baby. Furthermore, keeping track of the entire inventory I already have for the baby have resisted my urge to buy new things.

This is because seeing an actual list of inventory is overwhelming and it will make you think twice to add more to it.

With the baby expenses under control, the only thing I had to focus on was ensuring enough cash flow by continuing to look for work, invest, and possibly build a successful passive income stream (which is the reason why I started this blog – to explore those opportunities.).

In any case, having a baby tends to give parents newfound superpower. Once you embrace a sweet, fragile baby in your arms, you will forget all of the barriers to life and focus only on what matters.

As for me, I unlocked the superpower to stay laser focused on my goals while being sleep deprived. Such is the joy of parenting and I will stop at nothing to provide the best care for my Baby Bear.

Therefore, FI is truly the key to having more freedom, and freedom is always worth fighting for.

Have you heard about the FIRE movement? Do you value being financially independent and quit work early or do you prefer to work closer to standard retirement age? If you prefer the former, what can we do to accelerate FI?

FIRE up this PIN

Hello,

What a great post. I hadn’t come across the 4% rule before.

As someone who made very few financial preparations for retirement (“oh, I’ll never want to stop working”) I hope all younger readers will listen to me when I tell you that when you see your more prudent friends enjoying their retirement and financially free, you WILL feel a twinge and wish you’d done more.

I’ve been self-employed and worked hard and saved hard all my life, and have a comfortable life-style and debt-free, while I am still working. However, when I look to the future and fear that I may become ill or infirm and no longer able to work OR care for myself, it’s a bleak thought.

My Dad is 97 and needs a full-time live-in carer. I can tell you that is NOT CHEAP. But happily he’s financing it with the proceeds of the business he ran for 70 years. My sister and I are running it for him now. If he hadn’t done all that hard work in the past, goodness knows where we’d all be.

Can we coin a new term for me and others who missed the boat and having to catch up? FIRL – Financial Independence Retire Late!

We’re so lucky in this Internet age that we can run part-time online businesses to build up income while still working!

Joy Healey – Blogging After Dark

Thank for opening up and giving young readers a wise advice. I’m also glad that your dad has passed on his business to you. This is actually one of the reasons that motivated me to start this blog – to potentially pass down something of value to the next generation. It’s true that with today’s digital age, it has gotten so much easier and affordable to create an online business! I really appreciate your comment and sincere thoughts.

Thanks for taking the time to track the cost of having a baby, I think it’s one of those “taboos” that FIRE blogs tend to overlook.

As a FIRE blogger myself, being 34, I was of course also wondering how much having a baby would set me back, and it’s comforting to see a frugal person can still remain frugal with a child!

Hello, glad to meet another FIRE blogger! 🙂

Yes, the frugal bones runs deep in us haha. But with our baby, we were not aiming to be frugal actually, but to be more minimalist as we don’t want to accumulate too many baby items. We are expats in Switzerland so we need to keep it simple to avoid having headaches the day we move back to the states. The end result: Less junks and less spending!

Thanks for stopping by this blog! I’ll check out yours 🙂

I have never heard of the FIRE concept before reading this, but it is certainly interesting and enlightening. Job security is a thing of the past, it seems. So achieving financial independence is a really big deal. Thank you for sharing. I am saving this to begin really looking at my budget and finding ways to save more money.

I’m glad you found this article enlightening. That’s how I felt when I first read about FIRE, too.

It’s awesome to hear that you’re taking action. I’ll be rolling out some new contents about budgeting and investment strategies in the near future. Stay tune!

Well I have to say that I definitely like this more modern version of FIRE than the traditional loose your job and income association! Great article! Financial freedom is on the horizon:)

Thank you! I actually enjoy working, it gives me purpose. The challenge is to find one that is actually ENJOYABLE.

I have 3 babies and I’m still striving for FI! (don’t think FIRE is possible anytime soon!). My main money goal for 2020 is to focus on my investments. Great informative post Mona. Love it.

Hi Minda, FI is a journey and you sound like you got your eyes on the prize (your investment). You can do it!

Great suggestion! Budgeting and finances is never easy on me, I always want to have an easier way to manage it. Your post is definitely helpful

Glad you found it helpful. My goal is to simply personal finance so that people won’t shy away from this important topic!

Thank you for breaking all of this down. I think everyone WANTS to retire early, but most people struggle to understand what is required in order to make that dream a reality. You’ve explained this in such an easy to understand and actionable way!

Thanks for the thoughtful and kind feedback, Britt. I hope to help more people see the simplicity in personal finance through this little blog! Stay tune.

What an awesome post! i hand’t heard of the fire movement but that’s something i’m really looking foward to. Being financially independent and be able to have a baby afterwards it’s my goal right know. This post really helped enlighten me, thanks for sharing!

Glad you found it useful! This is exactly the purpose of this blog: to enlighten others about financial independence! You can do it!

It’s absolutely a stunning method to help us to understand and achieve financial freedom. Thanks for sharing.

Yes, thank you Trinity Study for showing us the light! And thanks for your feedback as well! 🙂

I was a financial advisor for most of my life and never heard of FIRE. This is an amazing acronym. I really believe that we need to live our life to the fullest and plan for retirement. Some people work work and save save and when the time comes to retire they are scared or never had fun. You have written an amazing article.

Thanks Jerry! Same here, I’ve been working in finance all my life and only heard about FIRE after I quit my job to study the MBA – got a bit more time on my hand for self improvement. After that, I couldn’t stop thinking about it!

It really goes to show that when we put our heads down and work, work, work, we forget to live live live 😉 Thanks a lot for stopping by!

I love the FIRE movement. I listen to Afford Anything podcast. Is my dream to be financial independent. But is so hard…. I need to follow your advice.

Me too, it’s a great movement to follow! I also read Afford Anything’s blog – love her story!

I could kick myself for not starting earlier in life with an approach like this. Now that I am 52 I am scared of the future. I don’t see retirement happening anytime soon for me. I tell my young girls all the time to prepare for retirement when you are young with at least a 401k. These are fantastic tips to implement. I hope to reach the RE part but I don’t see it happening for me. I think I may be more of a FIRN. Financial Idiot Retiring Never! 🙂

Hey many thanks for your bold feedback! I think it’s quite revelating for the younger workforce (such as your daughters) to learn from your experience. To be honest, what really woke me up was seeing how my parents, older relatives, and experience colleagues get so shaken up by the prospect of losing their job and that’s mainly because they rely on it for a living. But the rules of the game have changed so much that job security is simply gone. We, in the younger age group, must now take our career and financial matters into our own hands.

I never heard of FIRN lol, but I certainly don’t think you’re it since you’re taking that necessary steps to encourage your daughters to save early (that’s not an idiot in my book!). I also wrote an article on reaching early retirement in case it might help.

Very helpful financial advice. I have to focus on this by 2020. Great post. Thank You!

Fantastic! Thanks for the visit!

Achieving FIRE with kids is not that simple. I know because I am a mom of 3. It also does not mean you should not try. We are working towards it as a family and I am sure if we keep on it, we will get there soon.

I hear ya! Kids certainly add another layer of challenges especially when it comes to healthcare and education costs. But we’ll get there!

I appreciate that you brought up some extra points on how to achieve financial independence with a baby- that certainly added a whole new dynamic for us!

Glad you agree!

Your final suggestion to stay on track is so important isn’t it? It’s great to have a plan but its also important to keep up with it consistently and even crush your goals.

You’re right! It’s not enough to just start the process but you gotta follow-through all the way to your goal (and even crush it, yes!).

This was a great post! It definitely is harder to plan financially with a baby. They cost a lot, but this plan makes it seem simpler!

Hi Katie, thank you! Actually, to my surprise having a baby doesn’t cost as much as I initially thought. I tracked my expenses for the first six months and it was about only $2K. I’m curious to see the full year expenses though.

Thank you for the financial advice. This is definitely my 2020 focus so this article will come in handy.

Hello Sandra, glad you found the information useful.